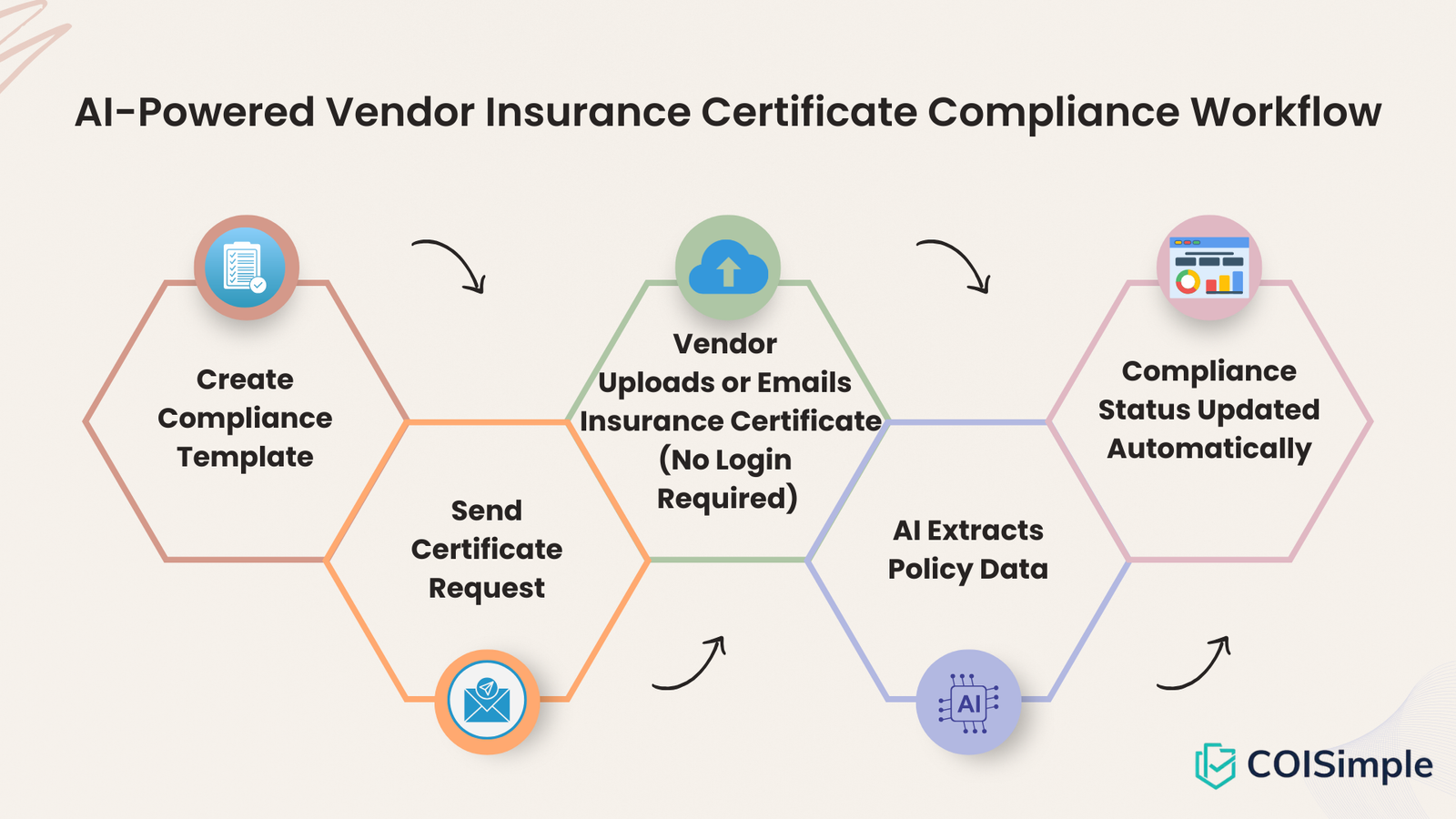

(A Practical Guide to Prevent Risk, Delays, and Compliance Gaps)

If you’re a contractor or property manager, collecting a Certificate of Insurance (COI) isn’t just paperwork — it’s your first layer of risk protection.

Too often, teams collect a COI, glance at the expiration date, and file it away.

That’s not enough.

Below is a practical, field-tested COI checklist you can use before approving any vendor or subcontractor.

✅ What Is a COI?

Most COIs are issued on the ACORD 25 Certificate of Liability Insurance form.

It summarizes:

- Coverage types

- Policy numbers

- Effective and expiration dates

- Limits

- Named insured

- Certificate holder

⚠ Important: A COI is evidence of coverage, not the policy itself.

📋 COI Checklist for Contractors & Property Managers

Use this checklist before marking a vendor “compliant.”

1️⃣ Named Insured Verification

✔ Is the legal business name correct?

✔ Does it match your contract/vendor agreement?

✔ Is it an LLC, Inc., or DBA as expected?

Why this matters:

If the name doesn’t match the contract, coverage disputes can arise.

2️⃣ Policy Effective & Expiration Dates

✔ Are all policies currently active?

✔ Do the dates cover the full contract term?

✔ Are any policies expiring within 30–60 days?

Best Practice:

Start renewal requests 45 days before expiration to prevent gaps.

3️⃣ Required Coverages Present

Typical required coverages include:

- Commercial General Liability (CGL)

- Workers Compensation

- Commercial Auto Liability

- Umbrella / Excess Liability

- Professional Liability (if applicable)

- Cyber Liability (if applicable)

✔ Confirm each required coverage appears on the COI

✔ Confirm “occurrence” vs “claims-made” if relevant

4️⃣ Limits Meet Requirements

This is where many teams miss critical details.

Common minimum limits:

| Coverage | Typical Minimum |

| General Liability | $1M per occurrence / $2M aggregate |

| Workers Comp | Statutory |

| Employers Liability | $500K–$1M |

| Auto Liability | $1M combined single limit |

| Umbrella | $1M–$5M |

✔ Do per occurrence limits match your template?

✔ Does aggregate meet requirement?

✔ Does umbrella properly sit over primary policies?

If limits are short, document it clearly before approval.

5️⃣ Required Endorsements

Most contracts require:

- Additional Insured

- Waiver of Subrogation

- Primary & Non-Contributory

- Completed Operations (if construction-related)

✔ Are boxes checked on the COI?

✔ If required, request endorsement pages — not just certificate wording

✔ Confirm Additional Insured is issued on a proper endorsement form (CG 20 10, CG 20 37, etc.)

Important:

COI wording alone does not guarantee endorsement issuance.

6️⃣ Certificate Holder Information

✔ Is your company listed correctly?

✔ Is address correct?

✔ Are special contract requirements included in the description box?

If the certificate holder is wrong, request re-issuance immediately.

7️⃣ Description of Operations Section

This section often includes:

- Project name

- Property address

- Additional insured wording

- Contract references

✔ Does it reference your specific project?

✔ Is project-specific coverage required?

✔ Are multiple locations listed if needed?

8️⃣ Carrier Financial Rating

✔ Is the insurance carrier rated A- or better (if required)?

✔ Is it a recognized carrier?

For large property portfolios, carrier stability matters.

9️⃣ Watch for Red Flags

🚩 Handwritten modifications

🚩 Expiration dates very close to today

🚩 Missing policy numbers

🚩 Coverage marked “Claims Made” without retro date

🚩 COI issued by vendor instead of broker

🚩 Policy effective date after work has already started

These require clarification before approval.

🏗 Special Notes for Contractors

If you are a general contractor:

- Require COIs from every subcontractor

- Track policies individually

- Tie compliance to job site access

- Re-verify coverage before final payment release

Many construction claims arise from uninsured subcontractors.

🏢 Special Notes for Property Managers

If you manage:

- Multi-family properties

- Commercial buildings

- Retail centers

- HOAs

Ensure:

- Vendors working on-site carry Workers Comp

- Landscaping, roofing, HVAC, and electricians carry proper GL + Auto

- Snow removal vendors have adequate umbrella coverage

- Tenant improvement contractors meet property insurance standards

📊 Pro Tip: Don’t Just Collect — Track

Collecting a COI is step one.

Tracking expiration, renewal, and compliance status is step two.

To reduce risk:

- Store policies individually

- Automate renewal reminders

- Document exceptions

- Keep an audit trail of approvals

Final Thoughts

A strong COI checklist protects:

- Your business

- Your property

- Your investors

- Your clients

COIs should not be treated as a checkbox exercise.

They are a risk management control system.

If you use this checklist consistently, you’ll:

- Reduce renewal chasing

- Prevent coverage gaps

- Avoid uninsured claims

- Strengthen contract enforcement

And most importantly — you’ll sleep better knowing your vendors are properly insured.